The Great Inversion: $690 Billion Is Pouring Into the Least Defensible Layer of the AI Stack

Authors:

Felix Kim & Redrob Research Labs

Date:

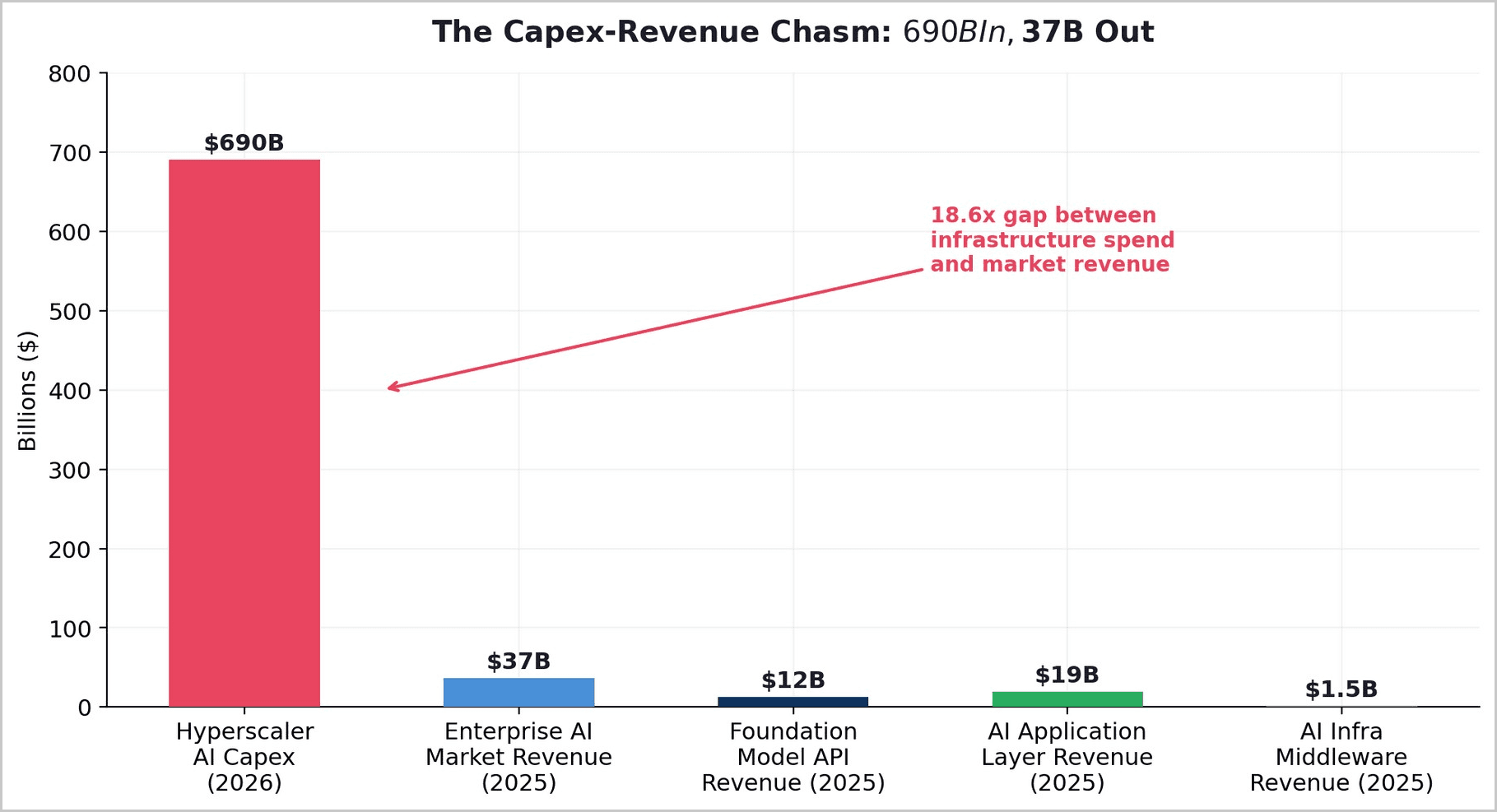

In 2026, the five largest US cloud and AI infrastructure providers will spend approximately $690 billion on capital expenditure — nearly all directed at AI compute, data centers, and networking. The enterprise AI market they serve generated $37 billion in revenue in 2025. This 18.6x gap between infrastructure investment and market revenue is not a temporary phase of front-loaded spending. It is a structural misallocation driven by a fundamental misunderstanding of where value and defensibility concentrate in the AI stack.

This paper presents evidence that the AI industry is experiencing a Great Inversion: capital is flowing overwhelmingly to the bottom of the stack (foundation models, chips, data centers) while actual value creation, margin capture, and competitive defensibility concentrate at the top (application layer, agentic orchestration, vertical workflows).

Foundation models exhibit classic commodity behavior — prices have fallen 98.75% in three years, benchmark leadership changes monthly, and no provider has established a durable lead. Meanwhile, the agentic layer — where AI systems autonomously plan, execute, and coordinate multi-step workflows — is creating the deepest moats in technology: persistent memory, proprietary workflow logic, and compounding data advantages that strengthen with every interaction.

1. The $690 Billion Question

The numbers are staggering. Amazon plans $200 billion in capex for 2026. Alphabet: $175-185 billion. Meta: $115-135 billion. Microsoft: $120 billion or more. Oracle: $50 billion. Combined, these five companies alone will spend $660-690 billion on infrastructure in 2026, the vast majority directed at AI. Meanwhile, OpenAI has announced roughly $1 trillion in infrastructure deals with partners including NVIDIA, Oracle, and Broadcom. Big tech companies issued $100 billion in bonds in 2026 alone to fund AI capex.

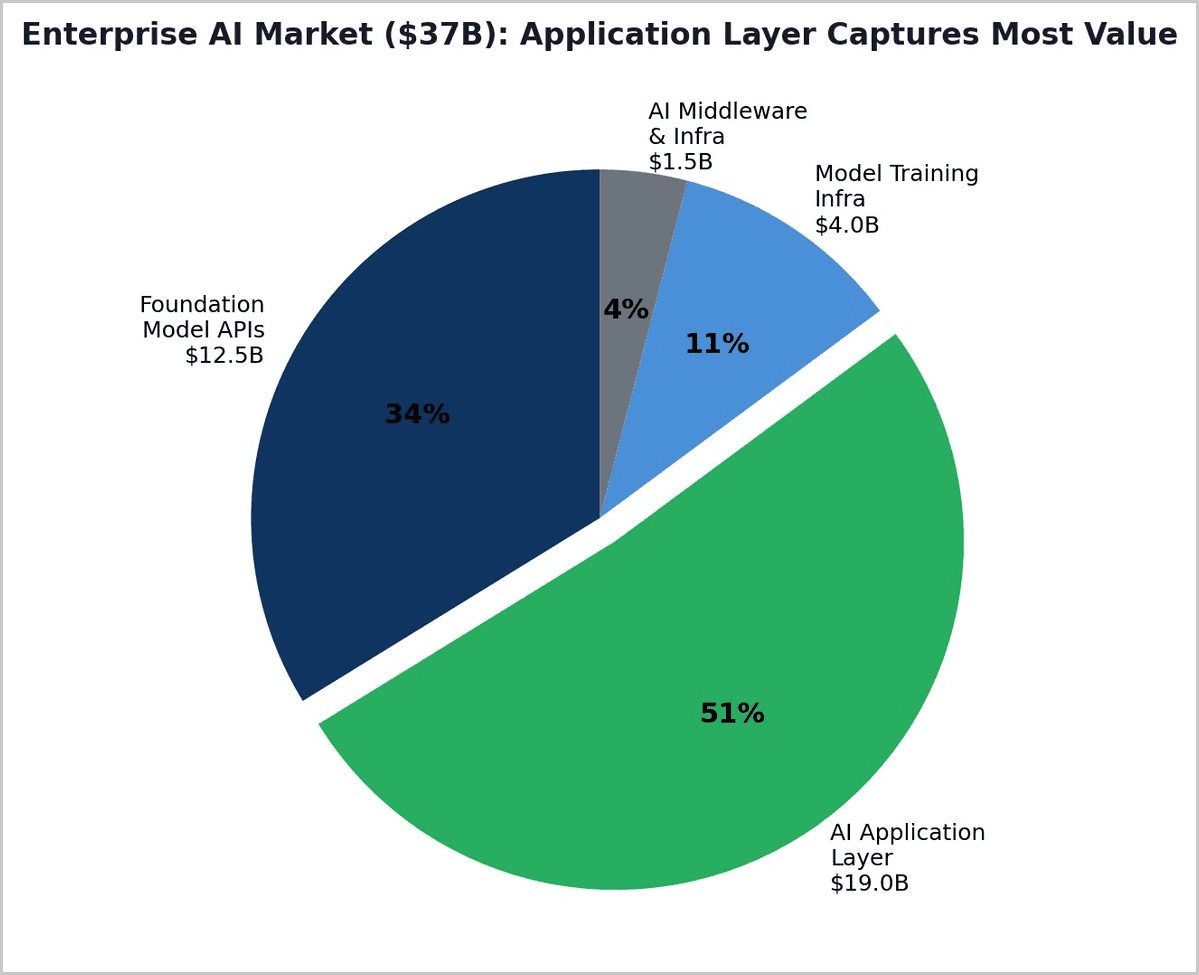

Against this spending, the entire enterprise AI market generated $37 billion in revenue in 2025. Microsoft's targeted $25 billion in AI-related revenue for fiscal 2026 pales against its $97.7-150 billion in capex. The ratio of infrastructure investment to market revenue is 18.6x — a gap that represents a fragile equilibrium where the entire supply chain hinges on the last link: the customer.

The question is not whether this spending will generate returns. Some of it will. The question is where in the AI stack those returns will concentrate — and whether the companies spending the most are building at the layer where value actually accrues.

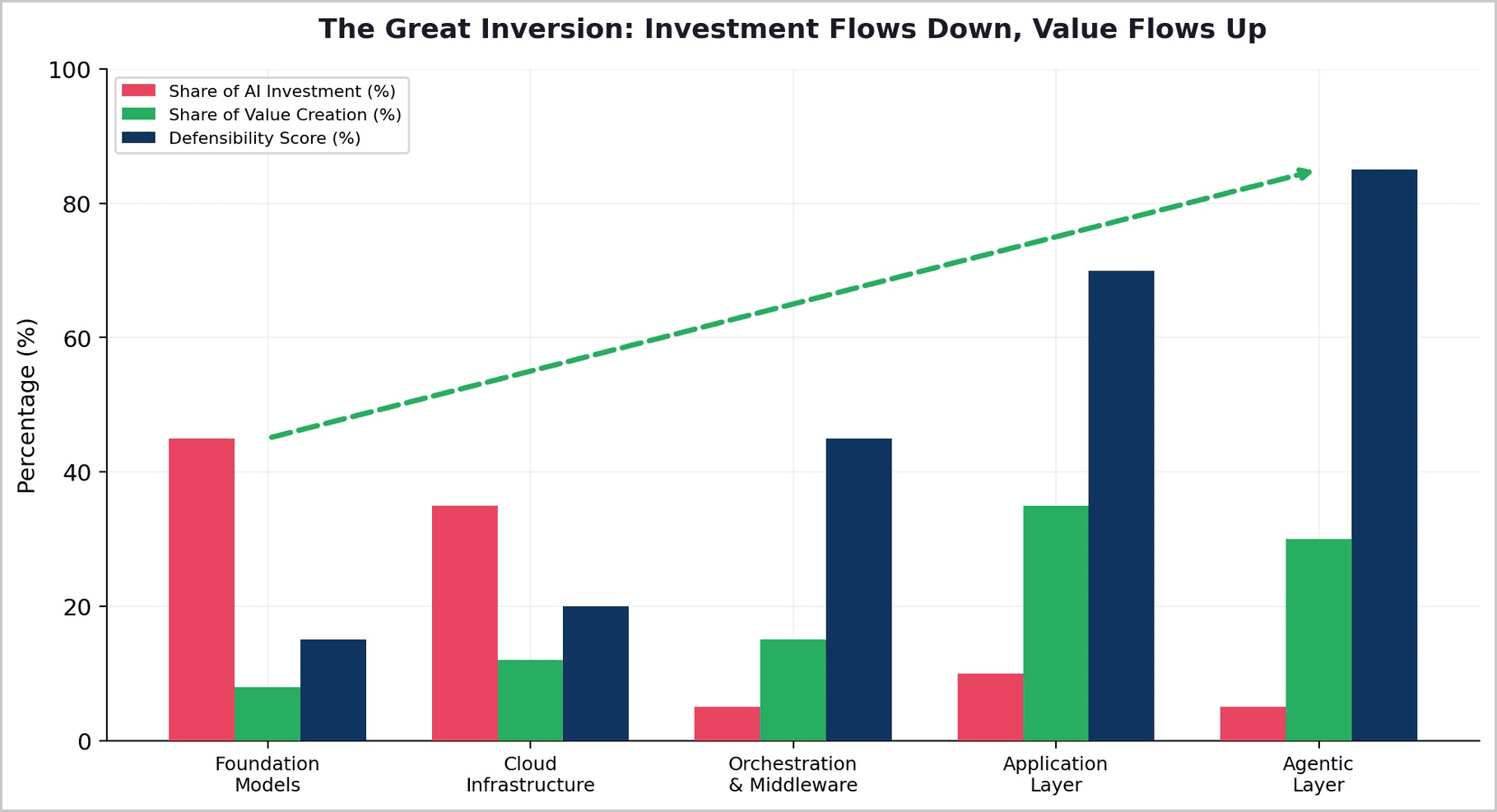

2. The Stack Is Inverting

The AI stack can be decomposed into five layers: foundation models, cloud infrastructure, orchestration/middleware, applications, and agentic systems. Investment concentration and value capture are moving in opposite directions across these layers.

At the foundation layer, investment is highest but defensibility is lowest. Models commoditize within months of release. Pricing collapses as competitors match capabilities. Anthropic cut prices by 67%. Google slashed rates 70-80%. OpenAI has repeatedly reduced costs on successive models. This is textbook commodity behavior — and a terrible place to build a moat.

3. Foundation Models: The Commodity Trap

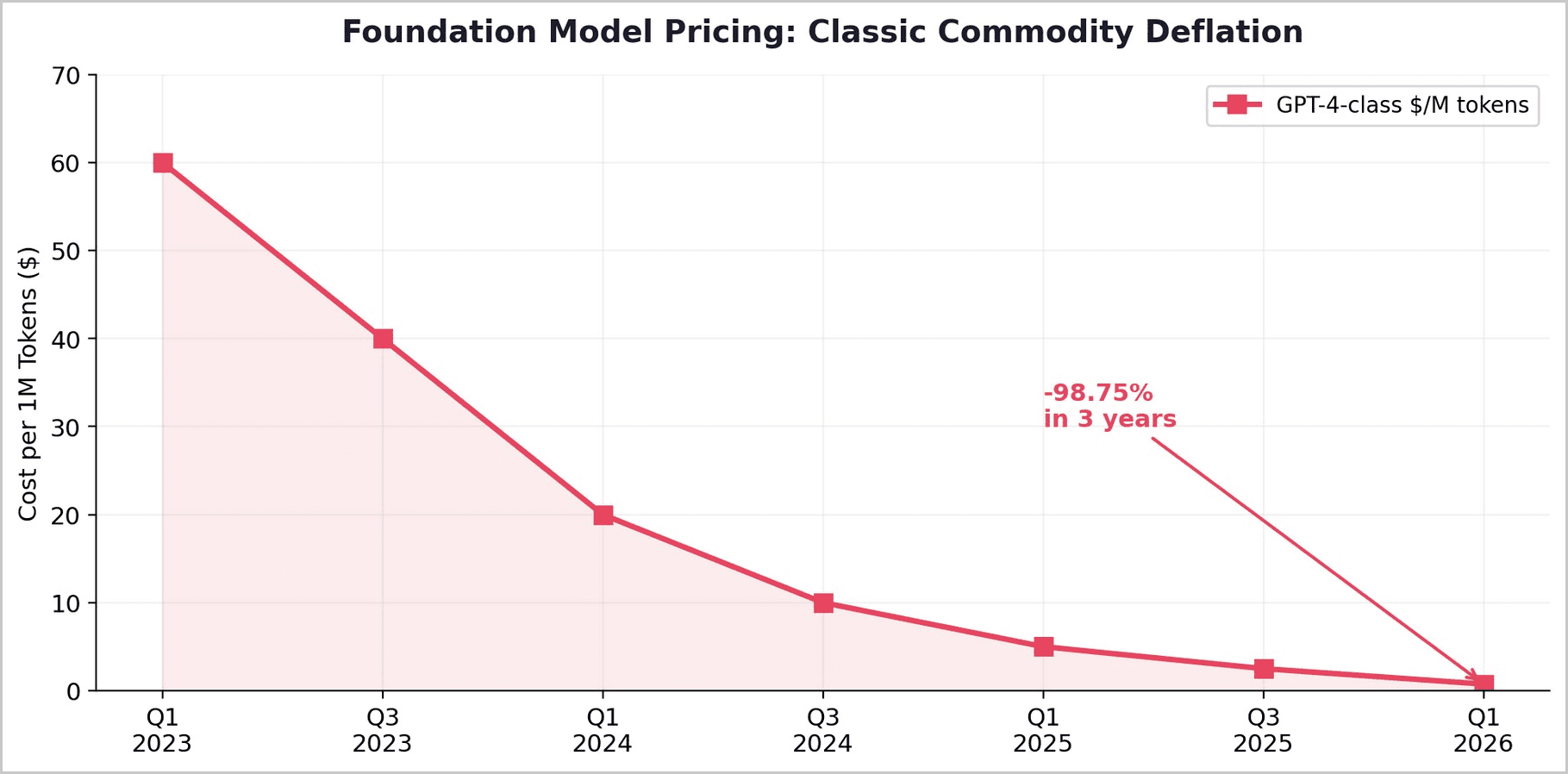

The evidence for foundation model commoditization is now overwhelming. Prices for GPT-4-class inference have fallen from approximately $60 per million tokens in early 2023 to under $1 in early 2026 — a 98.75% decline in three years.

The foundation model market is beginning to exhibit classic signs of commoditization. When one company introduces agentic capabilities, the others follow within months. Benchmark leadership changes constantly, with no provider establishing a durable lead.

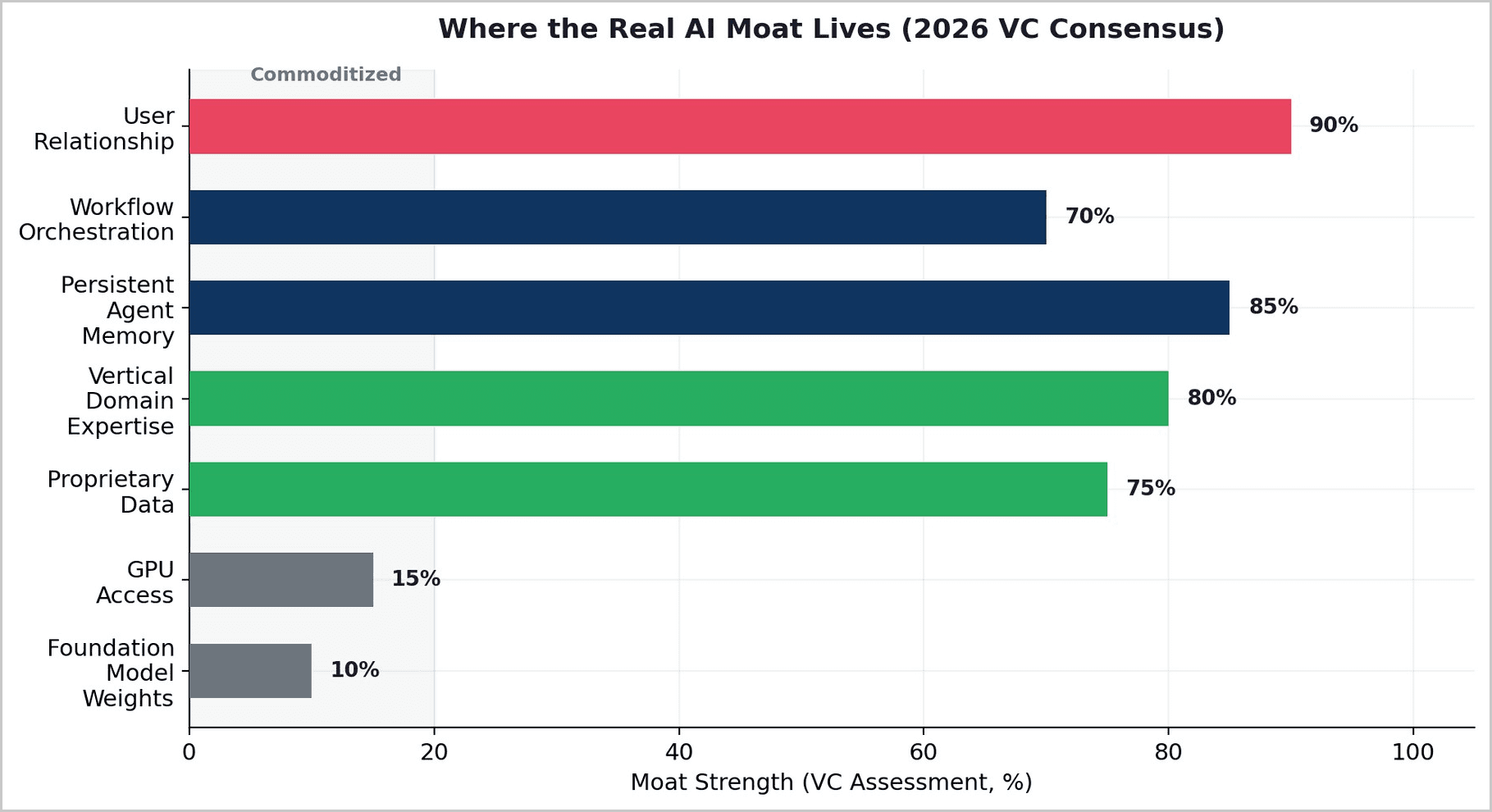

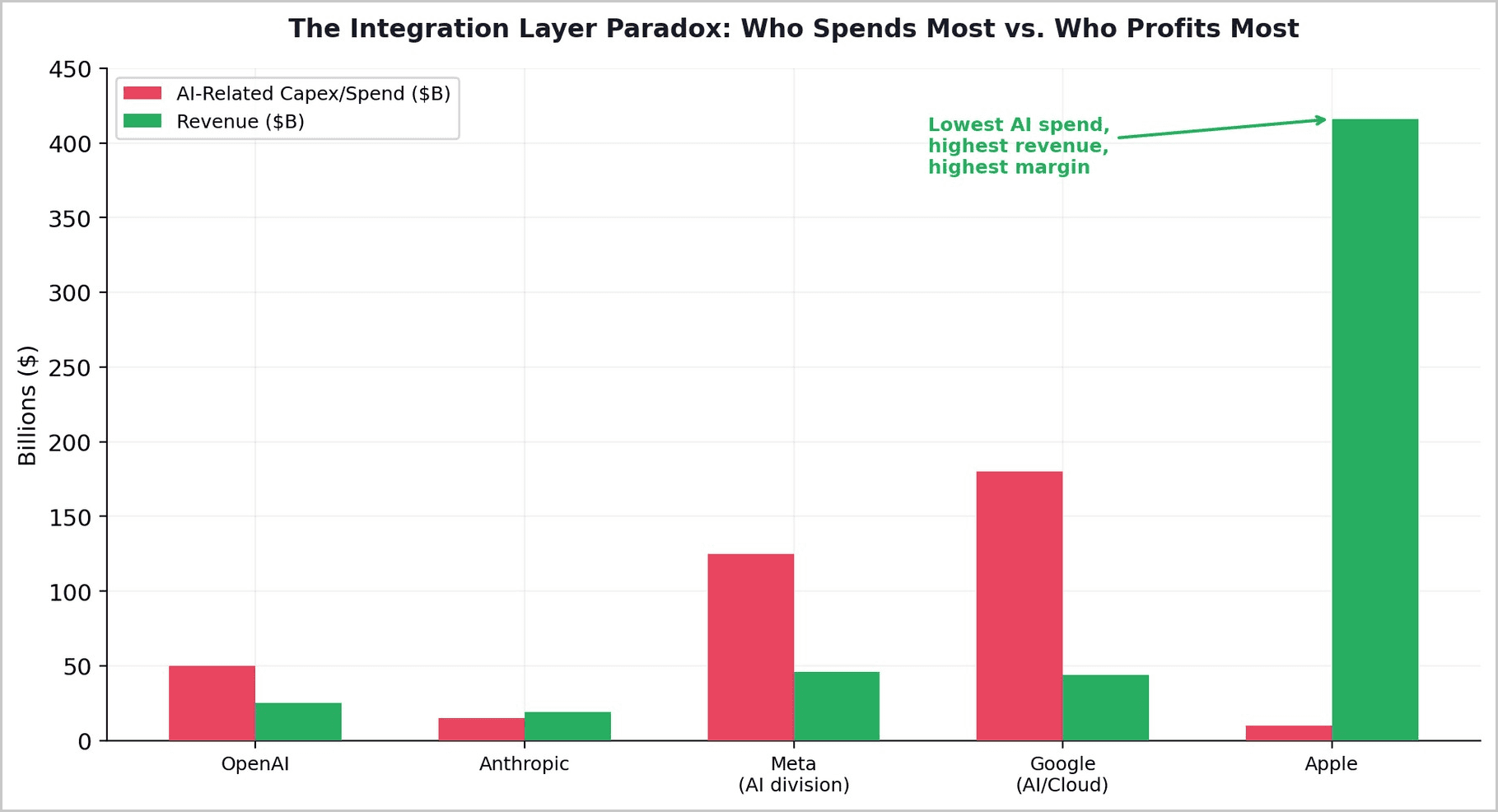

Apple's response is instructive. While competitors pour hundreds of billions into foundation model training, Apple sits on $130 billion in cash, recording $416 billion in revenue with nearly $100 billion in profit. Its strategy: source models from whoever is best at any given moment, wrap them in Apple's privacy architecture, and integrate across the ecosystem. Own the experience, outsource the commodity. Apple is not building the engine. It is curating the best available engine and integrating it into the layer where value actually concentrates: the user relationship.

3.1 Even Among Foundation Providers, No Moat Holds

The most striking evidence of foundation model commoditization is the volatility of enterprise market share among the providers themselves. Anthropic surprised industry watchers in 2025 by unseating OpenAI as the enterprise leader, capturing an estimated 40% of enterprise LLM spend — up from just 12% in 2023. Over the same period, OpenAI lost nearly half its enterprise share, falling from 50% to 27%. Google surged from 7% to 21%. If even the market leader cannot hold its position for 18 months, the foundation layer is not a moat — it is a revolving door.

3.2 The Cursor Proof: Application Layer Beats Infrastructure Incumbents

The most instructive case study of 2025-2026 is Cursor, a code editor built on top of commodity foundation models. GitHub Copilot, backed by Microsoft's infrastructure dominance, had every structural advantage: entrenched distribution, deep enterprise relationships, and privileged access to OpenAI models. Cursor beat it by building at the application layer. It shipped better features faster — multi-file editing, diff approvals, natural language commands — and its model-agnostic approach let developers adopt frontier models the moment they launched, rather than being locked to a single provider.

Cursor scaled to a $2 billion revenue run rate. The lesson is precise: the company that owned the infrastructure (Microsoft/GitHub) lost share to the company that owned the user experience and workflow integration. The model was interchangeable. The application layer was not.

The pattern: AI-native startups captured $2 in revenue for every $1 earned by incumbents in 2025 — 63% of the enterprise AI market, up from 36% the prior year. At least 60 AI-native products have reached $100M ARR, with 50+ expected to reach $250M by end of 2026. A lean team of 3-5 at the application layer now accomplishes what 20+ engineers do at the infrastructure layer.

4. The Agentic Layer: Where the Real Moat Lives

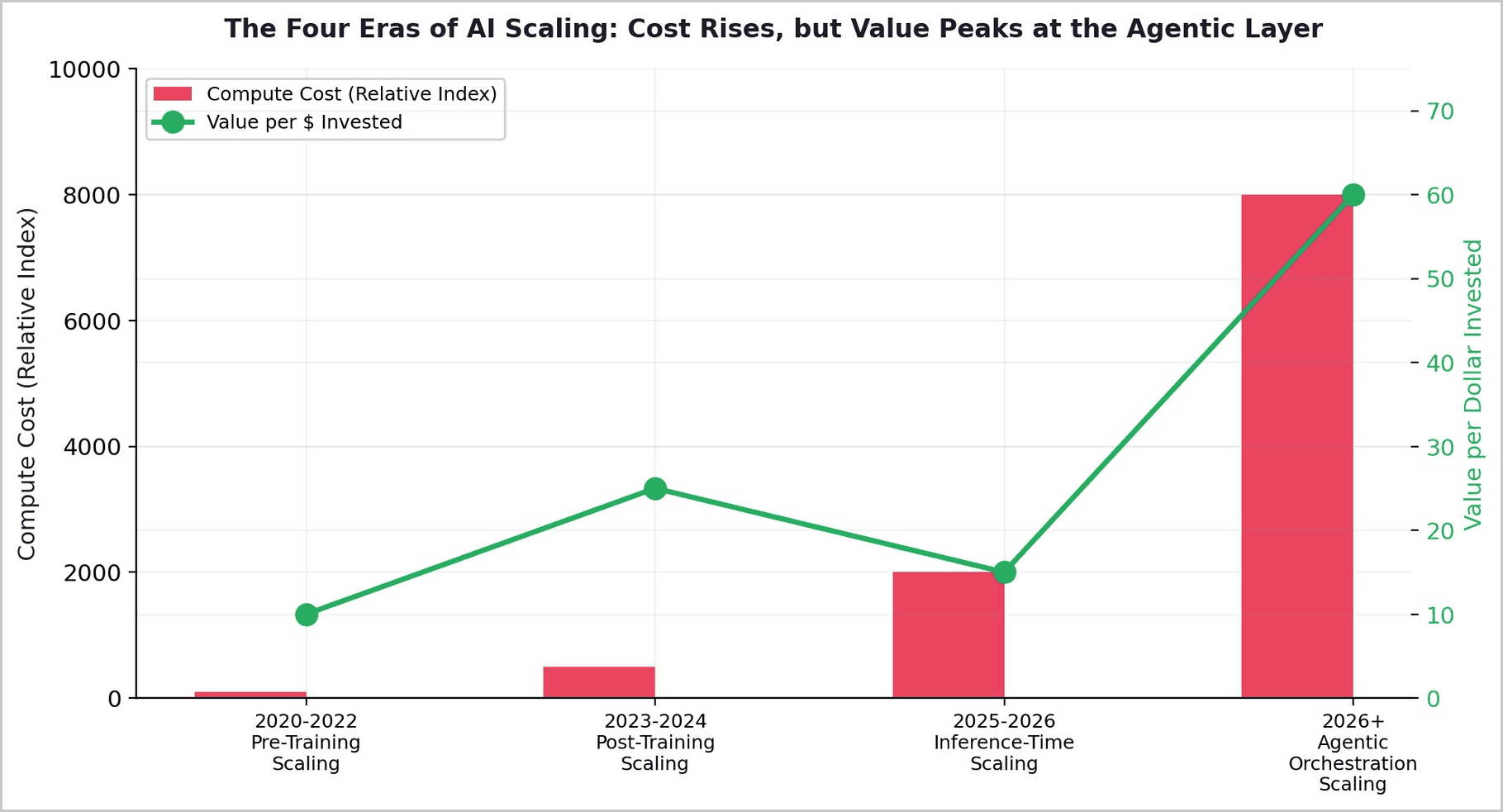

The shift from chatbots to agents is the most consequential architectural change in the AI industry since the transformer itself. In 2023-2024, AI was assistive: it helped humans complete tasks. By 2025-2026, AI is becoming operational: agentic systems autonomously plan, execute, and coordinate multi-step workflows with minimal human oversight. This transition has profound implications for where value accrues in the stack.

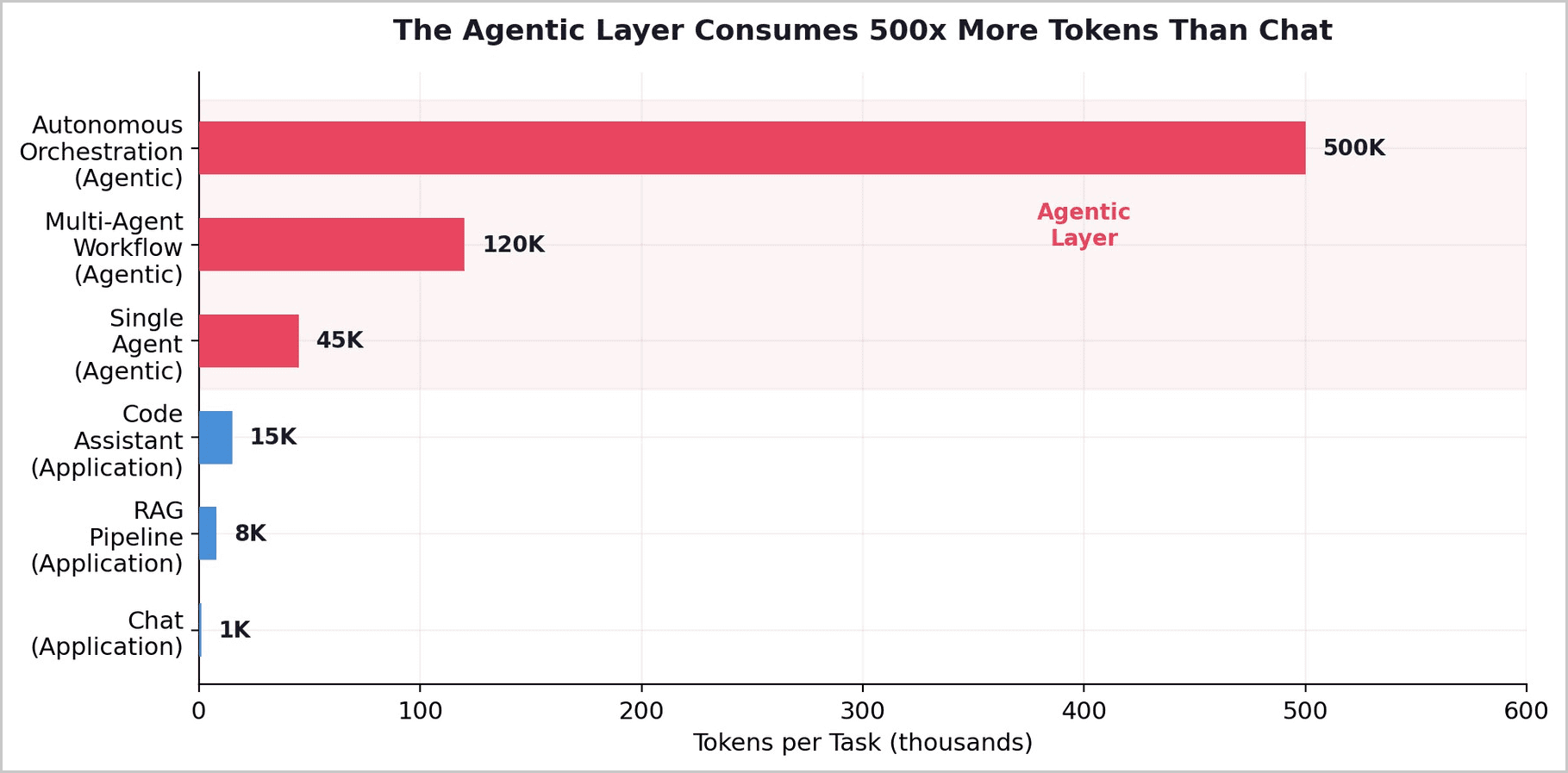

Agentic systems consume 50-500x more tokens per task than simple chat interactions. A single agent workflow burns 45,000 tokens. Multi-agent orchestration consumes 120,000. Fully autonomous orchestration systems can consume 500,000 tokens per task.

But the token consumption is not the strategic point. The strategic point is that agentic systems create moats that foundation models cannot. The strategic value lies not in building the agent's brain, but in defining and standardizing the tools those agents use. The true competitive advantage belongs to enterprises that have meticulously documented, secured, and exposed their proprietary business logic as high-quality, agent-callable APIs.

VCs now explicitly reject foundation-model pitches. The market has spoken: models are infrastructure, not moats. The moat is in what you build on top of them.

4.1 The Wrapper Era Is Dead. The Vertical Era Has Arrived.

In the early 2020s, startups achieved speed-to-market by wrapping existing LLMs with a thin UI. By 2026, that strategy is no longer viable. The wrapper era has collapsed under the weight of commoditization, as foundation models themselves integrate the very features startups once pitched as unique value propositions. What replaced it is vertical AI — smaller, domain-specific systems with deep context, privacy protections, and guaranteed accuracy for specific industries.

Bessemer Venture Partners proposed a thesis that vertical AI has the potential to eclipse even the most successful legacy vertical SaaS markets — and their conviction has only strengthened. Healthcare alone captures nearly half of all vertical AI spend at approximately $1.5 billion, more than tripling from the prior year. Harvey, an AI legal assistant, raised $600 million to reach an $8 billion valuation. The pattern is consistent: the narrower and more domain-specific the application, the deeper the moat and the higher the margin.

5. The Apple Thesis vs. The OpenAI Thesis

The contrast between Apple and OpenAI crystallizes the Great Inversion in a single comparison. OpenAI has raised enormous sums at sky-high valuations, projecting cumulative losses of $115 billion through 2029. Its gross margin is 33%, compressed by inference costs that consume revenue faster than it grows. It is building at the bottom of the stack — the most commoditized, most capital-intensive, least defensible layer.

Apple, by contrast, spent a fraction on AI, generated $416 billion in revenue, and earned nearly $100 billion in profit. Its AI strategy is to treat foundation models as interchangeable commodities, source the best one at any moment, and invest in the integration and experience layer where switching costs are highest. Apple is building at the top of the stack.

This is not to say Apple's strategy is risk-free. But it illustrates a principle that the AI industry is slowly learning: in a world where foundation models commoditize, the value accrues to whoever controls the user relationship and the orchestration intelligence — not whoever trained the biggest model.

6. Implications: Building at the Right Layer

6.1 For Enterprises

The enterprise lesson is clear: do not overinvest in proprietary foundation models or bespoke GPU clusters. Instead, invest in the orchestration and application layers where switching costs are highest and value capture is greatest. Use multi-model routing to commoditize the foundation layer — routing simple queries to cheap models and complex reasoning to frontier models. Build persistent memory, domain-specific knowledge graphs, and workflow automation that compounds in value over time.

6.2 For Emerging Markets

For emerging markets, the Great Inversion is liberating. The most expensive layer of the AI stack — foundation models — is the one you can get for free. Open-weight models now match frontier performance. The layers where real value concentrates — applications, agentic orchestration, vertical domain expertise, multilingual optimization — are the layers that require market knowledge and operational excellence, not capital. Application-layer seed rounds average $2-5M. Revenue per employee is 300% higher than traditional SaaS.

This means a team in Mumbai with deep domain expertise in Indian financial services and access to local language data can build a more valuable AI application than a team in San Francisco with 10x the GPU budget but no local context. Vertical AI thrives on domain specificity — and no one has more domain specificity in Indian healthcare, Southeast Asian logistics, or African mobile banking than the people who live in those markets.

6.3 For the AI Industry

The $690 billion capex wave will not be wasted entirely — it is building the infrastructure substrate on which the AI economy will run. But the returns on that infrastructure will not accrue primarily to those who built it. They will accrue to those who build the most valuable systems on top of it — just as the returns from internet infrastructure ultimately accrued not to the telecom companies that laid the fiber, but to the application companies that built on it.

7. Conclusion

The Great Inversion is the defining structural feature of the 2026 AI economy. $690 billion flows to the bottom of the stack — foundation models, GPUs, data centers — where commodity dynamics ensure that no player holds a durable advantage and margins compress toward zero. Even among foundation model providers, leadership is a revolving door: OpenAI lost half its enterprise share to Anthropic in 18 months. Meanwhile, the top of the stack — applications, agentic orchestration, vertical domain expertise — receives a fraction of investment but captures the majority of enterprise value, generates the highest margins, and creates the deepest competitive moats. AI-native startups capture $2 for every $1 earned by incumbents. 60+ products have reached $100M ARR in record time.

The foundation model was never the moat. The moat is the system that selects the right model for each task, routes queries intelligently across an ensemble, maintains persistent memory and workflow state, and wraps the intelligence in a user experience so deeply embedded in the customer's workflow that switching costs become prohibitive. This is the orchestration layer — and it is the most underinvested, most undervalued, and most strategically consequential layer of the AI stack.

The companies that will define the AI era are not those building the largest models. They are those building the smartest systems for deploying intelligence at the layer where value actually accrues — and doing so at cost structures that the entire world, not just the wealthiest 15%, can afford.

The engine matters less than the vehicle it powers. And the vehicle matters less than the road it drives on.

About Redrob Labs:

Redrob (redrob.io) builds large language models and AI tools for the next three billion users. Founded in 2018, the company operates a proprietary multi-model ensemble architecture delivering 90% of frontier performance at 5% of the cost - purpose-built for the unit economics of India and emerging markets. Headquartered in New York with offices in Seoul, New Delhi, and Mumbai. Backed by world-class VC firms. Redrob Labs is the research division of Redrob. Our work is published at redrob.io/research.