India Doesn’t Need 100 Million Factory Jobs. It Needs 100 Million AI Copilots.

FELIX

India Doesn’t Need 100 Million Factory Jobs. It Needs 100 Million AI Copilots.

By 2030, one in five working-age humans will be Indian. Only 5% are formally skilled. The conventional wisdom says India must industrialize. AI says otherwise.

In January 2026, China reported that births had collapsed 17% in a single year to 7.92 million - the lowest since 1949. Marriages plunged 20%. The American Enterprise Institute called it “population decline on a scale the world has never seen,” projecting China could lose 250 million working-age people by 2050. Demographers said the decline was “typically associated with famine or plague.”

Meanwhile, 3,000 kilometers to the southwest, India is adding 101 million people to its working-age population in the same decade. By 2030, one in every five working-age humans on Earth will be Indian. The demographic dividend window - that precious period when workers vastly outnumber dependents - will remain open only until roughly 2045-2050. After that, India ages rapidly too.

The conventional wisdom is that India must industrialize at scale to capture this dividend - building factories, creating manufacturing jobs, following the “Asian Tiger” path that lifted South Korea, Taiwan, and China. The government target: increase manufacturing from 16% to 25% of GDP. The implicit assumption: India needs 100 million factory jobs.

There is a problem with this plan. India has only 5% formally skilled workers - compared to 80% in Japan, 96% in South Korea, 68% in the UK, and 52% in the US. According to the Economic Survey 2024-25, 88.2% of India’s workforce is employed in low-competency jobs. Only 4.1% of working-age Indians have received formal training. The skills gap is not a detail to be addressed. It is the defining constraint of India’s economic future.

But here is the counterintuitive insight that almost nobody is discussing: AI does not require a skilled workforce to augment one. It IS the skill. And that changes the entire calculus of India’s demographic dividend.

1. The Great Demographic Divergence

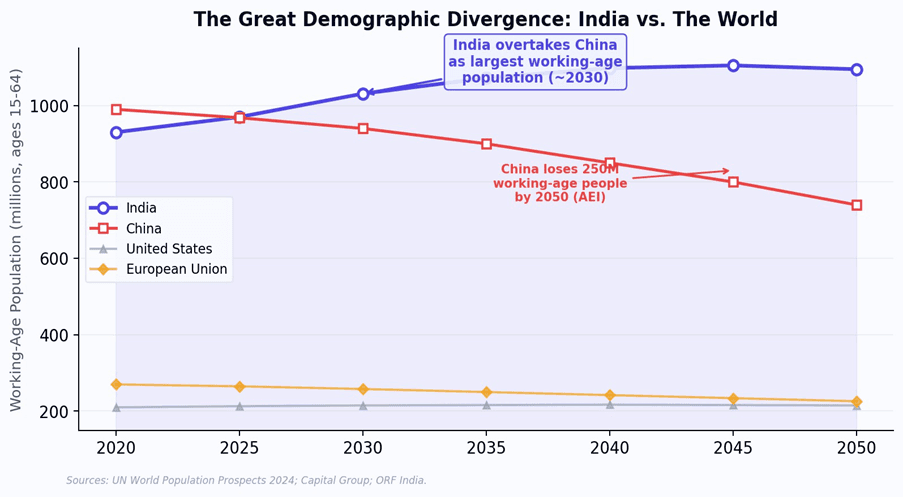

The numbers are historic. India’s working-age population (15-64) currently stands at approximately 970 million and will cross 1 billion by 2028. It will peak around 1.1 billion in the mid-2040s. No other major

economy is growing. China’s working-age population peaked in 2015 and is now shrinking by 6.6 million per year - with AEI projecting a loss of 250 million workers by 2050. Europe loses working-age people every year. Japan’s workforce has been contracting for two decades. The United States is effectively flat. India stands alone as the only major economy adding large numbers of working-age people for the next twenty years.

Figure 1: Working-age population trajectories. India crosses 1 billion workers while China faces what AEI calls a loss of 250 million working-age people by 2050 - a decline 'typically associated with famine or plague.'

India’s median age is 29.8 - compared to 40.2 in China, 38.5 in the US, and 44.6 in the EU. GDP per capita is projected to double from approximately $2,500 today to $5,000-5,700 by 2030, according to Bloomberg Economics and EY. India is already the world’s fourth-largest economy by nominal GDP and third-largest by purchasing power parity. Its digital economy reached $402 billion in 2022-23 (11.74% of GDP) and is projected to reach 20% of GDP by the late 2020s. The population is expected to peak at 1.7-1.8 billion in the 2060s and remain the world’s largest through the entire century. This is not a temporary advantage. It is a structural feature of the 21st-century global economy.

But a large, young population is not automatically an economic asset. It becomes one only if those workers are productive. And productivity requires skills that India’s workforce overwhelmingly lacks.

2. The 5% Problem: India’s Skills Gap Is Not What You Think

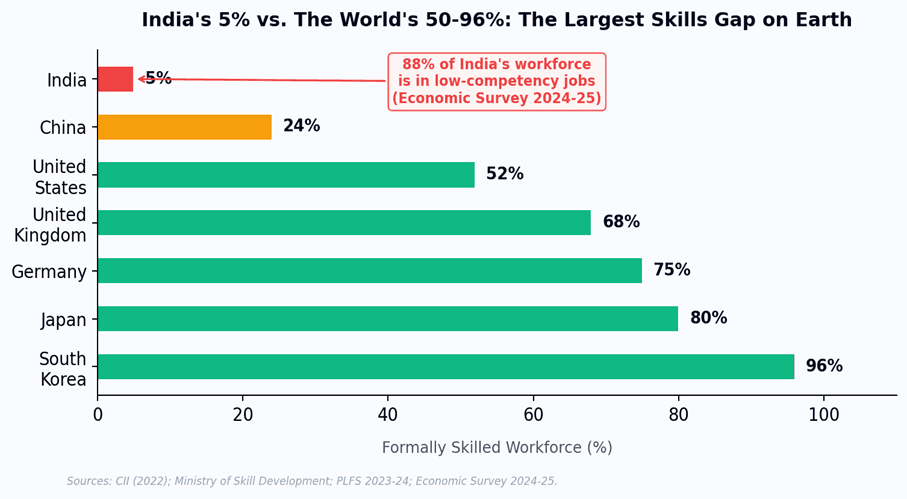

The headline statistic is brutal: only 5% of India’s workforce has received formal skill training. Compare this to South Korea (96%), Japan (80%), Germany (75%), UK (68%), US (52%), or even China (24%). India’s skilling capacity trains fewer than 7 million people per year - while 12 million enter the workforce annually. The gap compounds every year.

Figure 2: Formally skilled workforce as a percentage of total workforce. India's 5% is the lowest among all major economies.

The conventional response is to build more training centers, expand vocational programs, and push for apprenticeships. India’s Skill India Mission aims to do exactly this. But the math does not work. To reach even China’s modest 24% skilled workforce rate, India would need to formally skill an additional 104 million workers - roughly the population of Germany and France combined. At current training capacity, this would take over 15 years. The demographic dividend window does not wait that long.

“The question is not whether India can skill 100 million workers fast enough. The question is whether it needs to.”

3. The Leapfrog Pattern: India’s History of Skipping Stages

To answer that question, it helps to look at what India has done before when faced with seemingly insurmountable infrastructure gaps. The pattern is striking - and it suggests the conventional skilling approach may be asking the wrong question entirely.

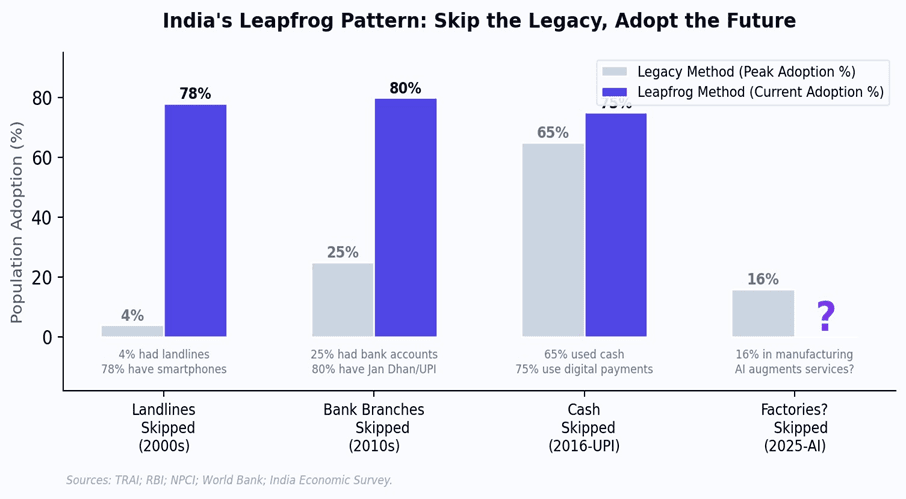

Landlines to mobile (2000s): India never built a comprehensive landline network. At peak, only 4% of the population had a fixed-line phone. Today, 78% have smartphones. India skipped an entire generation of telecommunications infrastructure.

Bank branches to digital (2010s): Rather than building hundreds of thousands of bank branches, India created Jan Dhan (500 million bank accounts opened in years, not decades) and UPI (Unified

Payments Interface). India went from 25% bank account penetration to 80% in under a decade - without the branch network that took Western countries a century to build.

Cash to digital payments (2016-present): UPI transactions grew from zero to over 14 billion transactions per month and $2.4 trillion annually in seven years. India now processes more real-time digital payments than the US, UK, and EU combined. Aadhaar digital identity covers 1.4 billion people - the largest biometric identity system on Earth.

Figure 3: India's pattern of skipping legacy infrastructure stages. The question mark: will AI allow India to skip factory-led industrialization?

The pattern is consistent: when India faces a structural constraint (no telecom infrastructure, no banking infrastructure, no payment infrastructure), it does not build the legacy system. It jumps to the next generation. The structural constraint it faces now - a massive, young workforce with only 5% formal skills - is the same type of problem. And AI is the same type of leapfrog technology.

4. AI as the Great Equalizer: Why Skills Gaps Stop Mattering

Here is the genuinely counterintuitive claim: AI does not augment skilled workers. It substitutes for the skill itself. A farmer with a smartphone and an AI assistant can access agronomic advice that previously required an agricultural extension officer with a university degree. A small business owner with an AI-powered accounting tool operates with the financial sophistication of a trained bookkeeper. A salesperson with an AI copilot writes emails, analyzes prospects, and prepares proposals at a level that previously required years of professional training.

This is fundamentally different from previous technology waves. The PC revolution required computer literacy. The internet required reading skills and English proficiency. Cloud software required trained operators. Each previous wave amplified existing skills - making skilled workers more productive while leaving unskilled workers behind. AI is the first technology that can deliver the skill itself, directly to the user, in their language, through a device they already own.

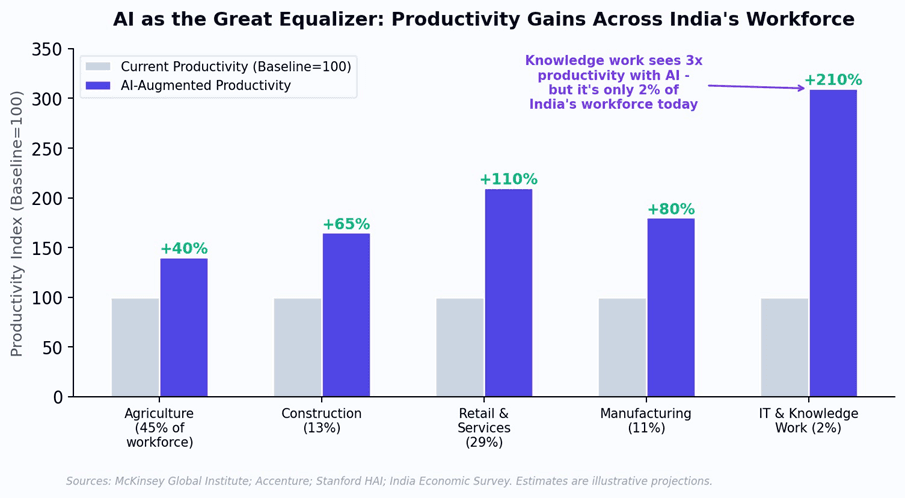

Figure 4: AI-driven productivity gains across India's workforce sectors. The largest gains come not from knowledge work (2% of workforce) but from augmenting the other 98%.

India’s 700 million smartphone users, UPI infrastructure, and Aadhaar digital identity system create the distribution rails. AI provides the capability layer on top. The combination means that for the first time, a productivity technology can reach the 88% of India’s workforce currently in low-competency jobs - without requiring them to spend years in formal training programs first.

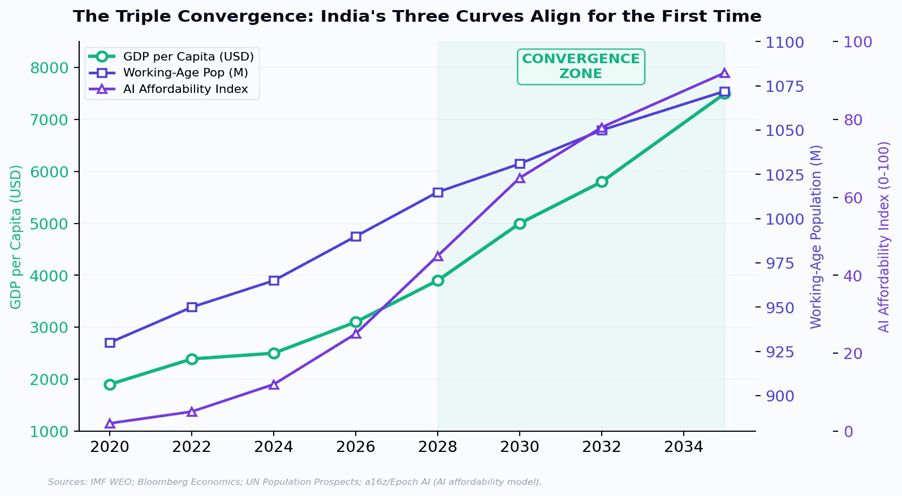

5. The Triple Convergence: Three Curves That Have Never Aligned Before

AI’s potential as a skill equalizer is clear. But potential is not destiny. What makes the current moment historically unique is not any single trend, but the simultaneous convergence of three curves that have never aligned before in any country:

Curve 1: The largest working-age population in history.

India is adding over 100 million workers this decade alone, with peak workforce size arriving in the mid-2040s - just as China’s workforce enters terminal decline.

Curve 2: The fastest per-capita GDP growth among major economies.

GDP per capita is doubling from ~$2,500 to ~$5,000 by 2030. The digital economy is projected to reach 20% of GDP by the late

2020s, up from 11.74% today.

Curve 3: AI becoming affordable at Indian price points.

As documented in our previous analysis of the Jevons Paradox, per-user AI costs are falling toward emerging market ARPU levels, with convergence expected around 2029. For companies with purpose-built architectures, this convergence is already achievable today.

Figure 5: The Triple Convergence - GDP per capita, working-age population, and AI affordability all rising simultaneously. This combination is historically unprecedented.

No country in history has had all three of these conditions at once. China had the demographic dividend but AI did not exist - and now its fertility rate of 1.01 means the window has permanently closed. The US has AI but its workforce is aging and its working-age population is flat. South Korea industrialized with skilled labor but now has the world’s lowest fertility rate (0.73) and its population is in terminal decline. Japan pioneered automation but did so while aging into a dependency crisis. India’s window is unique - and it is open now.

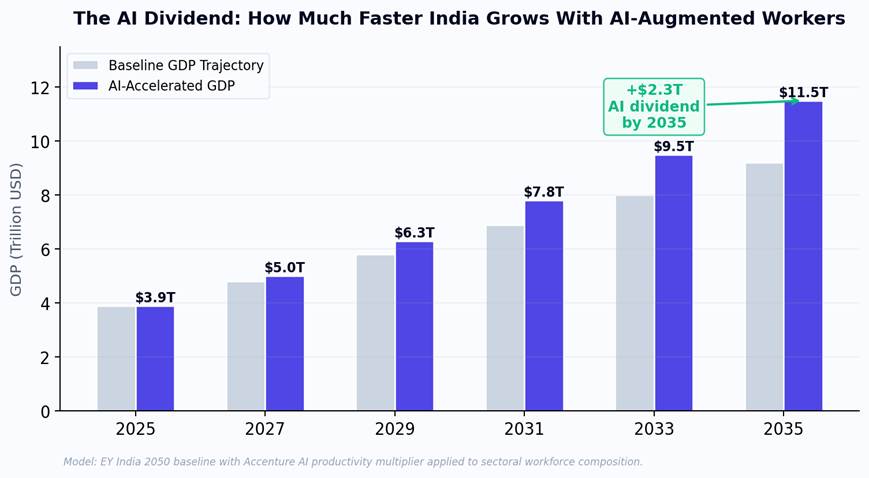

6. The $2.3 Trillion AI Dividend

If AI can multiply the productivity of India’s existing workforce – even partially – the GDP impact is enormous. Accenture estimates AI could add $957 billion to India’s economy by 2035. Our modeling, which incorporates the triple convergence dynamics and sector-specific productivity multipliers, suggests the cumulative AI dividend could reach $2.3 trillion in additional GDP by 2035 - representing the difference between a $9.2 trillion baseline economy and an $11.5 trillion AI-accelerated one.

Figure 6: India's GDP trajectory with and without AI-augmented workforce productivity. The AI dividend could reach $2.3 trillion by 2035.

The applications that will drive this are not the ones Silicon Valley is building. They are vernacular-language AI tutoring for 300 million students in 22 languages. AI-powered agricultural advisory that reaches 240 million farm workers through the smartphones they already own. Automated compliance and bookkeeping for India’s 63 million SMEs. AI-driven recruitment that matches skills rather than credentials across a labor force of 500 million. And the multiplication of India’s $250 billion IT services export industry - where 5 million workers could produce the output of 15 million with AI augmentation, fundamentally reshaping India’s position in the global knowledge economy. These are not niche use cases. They are the core of India’s economy.

7. Why Redrob Is Building for This Moment

Capturing the AI dividend in India requires a specific kind of architecture - one that most Silicon Valley AI companies are structurally incapable of building. It requires multilingual models that work in Hindi, Tamil, Bengali, and 19 other languages. It requires on-device inference that runs on $100 smartphones, not $1,000 laptops. It requires price points calibrated for a market where per-user revenue is measured in cents, not dollars. And it requires deep domain expertise in the sectors that actually employ India’s workforce - agriculture, construction, retail, and services - not just the 2% in IT.

Redrob is building the Android of LLMs precisely because this market cannot be served by the iPhone approach. A 5-model ensemble (Redrob 2B, Llama 3 8B/70B/405B, Llama 4 Maverick) running on AWS Bedrock, with a lightweight on-device model for smartphone deployment, is not a cheaper version of what OpenAI offers. It is a fundamentally different product for a fundamentally different market – one that is about to become the largest AI opportunity in the world.

India does not need to skill 100 million workers the old way. It needs to give 100 million workers an AI copilot. The companies that make this possible will not just participate in India’s demographic dividend – they will be the reason it gets captured at all.