Every government wants “sovereign AI.” But every technology era was won by the companies that controlled distribution, not the ones that invented the core technology. India’s real AI advantage isn’t a foundation model. It’s 1.4 billion Aadhaar IDs, 14 billion monthly UPI transactions, and 700 million smartphones.

In April 2025, the Indian government selected Sarvam AI to build India’s first sovereign large language model under the IndiaAI Mission. The company received access to 4,096 NVIDIA H100 GPUs at a government-subsidized data center. Krutrim, backed by Ola founder Bhavish Aggarwal, had already hit unicorn status. BharatGen, a consortium led by IIT Bombay, received roughly Rs 1,000 crore. In total, the government is now funding 12 organizations to build indigenous AI foundation models.

The narrative is compelling: India needs AI sovereignty. It cannot depend on American or Chinese models for its national AI infrastructure. It must build from scratch.

There is just one problem with this narrative. It has never been true for any technology era in history. Not once has the entity that invented the core technology captured the majority of the value. The value always accrues to whoever controls the distribution layer - the last mile to users. And India already has the most powerful AI distribution infrastructure on Earth. It just doesn’t know it yet.

1. The Pattern Nobody Talks About: Distribution Eats Technology

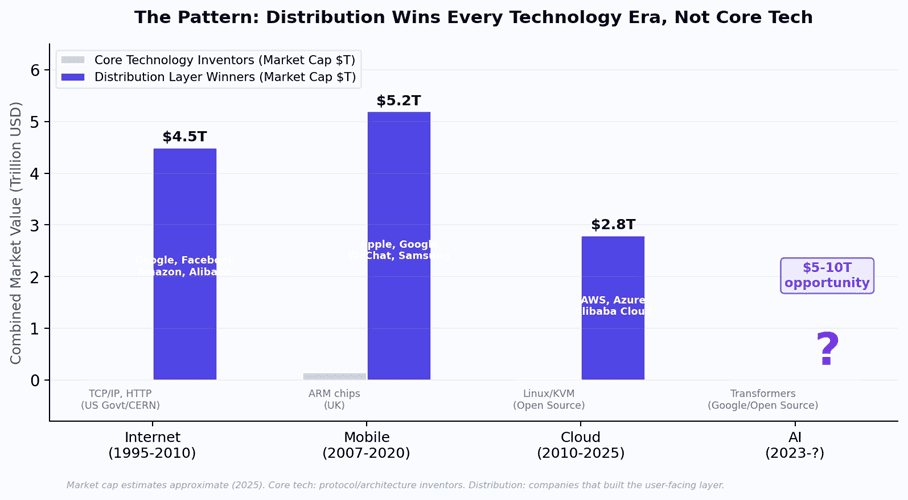

Consider the history carefully. The internet was invented by DARPA and CERN - neither of which captured meaningful commercial value. The commercial value went to Google, Facebook, Amazon, and Alibaba - companies that built the distribution layer on top of the same open protocols (TCP/IP, HTTP) that anyone could use.

The smartphone era followed the same pattern. ARM designed the chip architecture. Qualcomm built the modems. But the overwhelming majority of value went to Apple and Google - which controlled the distribution layers (iOS and Android). Samsung won by controlling the hardware distribution. None of them invented the core mobile technology.

Cloud computing was built on Linux and KVM - both open source. The value went to AWS, Azure, and Alibaba Cloud, which built distribution layers on top. And China’s tech dominance was not built by reinventing TCP/IP or ARM. It was built by WeChat (1.3 billion users), Alibaba ($1 trillion GMV), and Baidu - all of which ran on the same global infrastructure that everyone else used. China won distribution, not core technology.

Figure 1: In every technology era, the distribution layer captures 10-50x more value than the core technology inventors.

The pattern is remarkably consistent. The entity that invents the core technology almost never captures the majority of the value. The entity that controls how that technology reaches users captures nearly all of it. Foundation models are AI’s TCP/IP. They are essential infrastructure - and they are rapidly commoditizing.

2. Foundation Models Are Commoditizing Faster Than Any Previous Core Technology

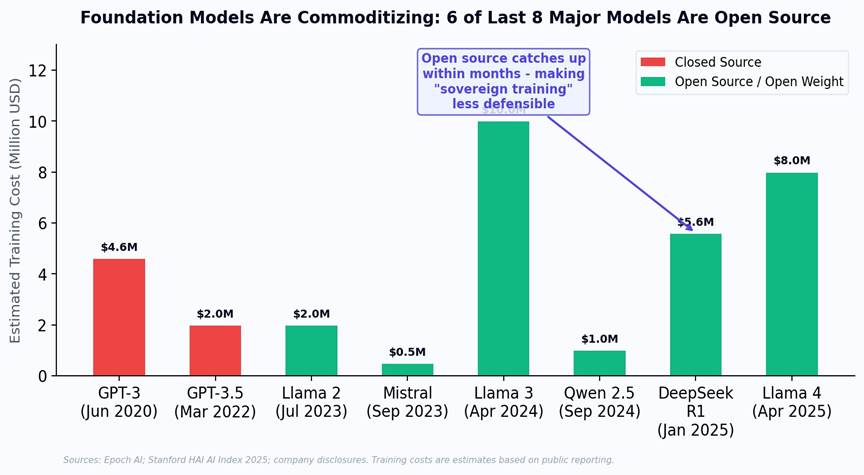

Six of the last eight major language models released globally are open source or open weight: Llama 2, Mistral, Llama 3, Qwen 2.5, DeepSeek R1, and Llama 4. When DeepSeek released R1 in January 2025, it demonstrated that frontier-class reasoning could be achieved at a fraction of the training cost of GPT-4 - sending Nvidia’s stock down $600 billion in a single day. The lesson was unmistakable: foundation models are commoditizing at unprecedented speed.

Figure 2: The open source wave. Six of the last eight major models are open source, making 'sovereign training from scratch' increasingly hard to justify economically.

This is directly relevant to India’s sovereign AI debate. Sarvam AI’s recent 105-billion-parameter model, trained from scratch on Indian data, is a genuine technical achievement - and its vision OCR scores 84.3% on benchmarks, beating Gemini 3 Pro and ChatGPT on Indian-language documents. Krutrim’s multilingual models push the frontier on Indic languages. This work matters enormously for national capability. But it exists in a context where open source alternatives improve every quarter. The real question is not whether India can build foundation models - it clearly can. The question is whether foundation models alone constitute a durable strategic advantage when the underlying technology is commoditizing this fast.

“Sovereign AI does not mean building your own transistor. It means controlling the last mile to your own citizens - before someone else does.”

3. Where Value Actually Accrues in the AI Stack

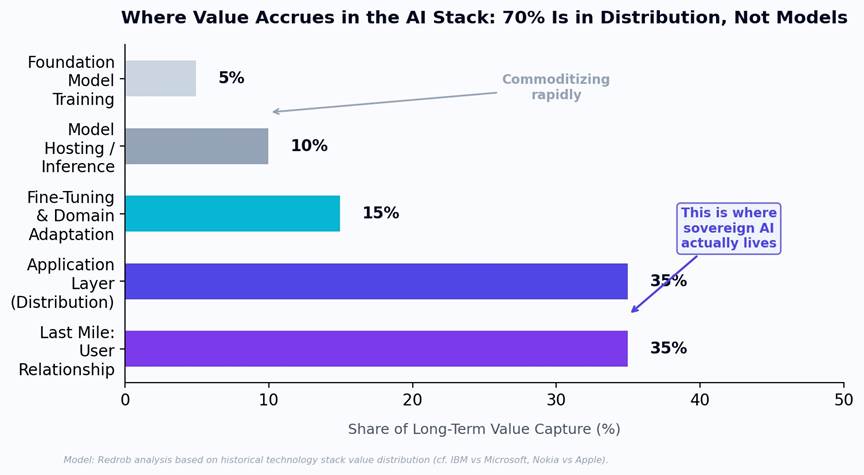

If foundation models are commoditizing, where does long-term value actually live? The answer follows the same pattern as every previous technology era: it lives in the layers closest to the user.

Figure 3: Value distribution across the AI stack. 70% of long-term value accrues to the application and user relationship layers - the distribution stack.

Foundation model training (5% of value): Increasingly commoditized through open source. Llama 4 is free. DeepSeek is free. Mistral is free. Training your own model from scratch costs $50-100M+ and delivers, at best, marginal performance improvement over what is already available for free.

Application layer + last-mile distribution (70% of value): This is where defensible moats are built. Domain-specific fine-tuning for Indian hiring practices, agricultural workflows, SME compliance, and vernacular customer service. Integration with UPI, Aadhaar, and India’s digital public infrastructure. Voice-first interfaces in 22 languages. On-device inference on the smartphones that India’s 700 million mobile users already carry. This is not a technology problem. It is a distribution problem.

4. India’s Hidden Advantage: The World’s Best AI Distribution Stack

Here is the counterintuitive insight that the sovereign AI debate is missing: India has already built the most powerful AI distribution infrastructure in the world. It just built it for a different purpose.

1.Aadhaar (1.4 billion digital identities):

The world’s largest biometric identity system provides a universal, authenticated user layer that no other country has at scale. Every AI service can authenticate, personalize, and deliver to a verified individual.

2.UPI (14 billion transactions/month, $2.4 trillion annually):

The world’s largest real-time digital payment system provides instant monetization infrastructure for AI services. A farmer can pay for AI crop advisory with the same phone tap that pays for groceries.

3.700 million smartphones:

The distribution endpoint already exists. No new hardware deployment needed. AI reaches users through the device they already carry.

4.22 official languages:

India’s linguistic diversity, often cited as a barrier, is actually a distribution moat. A model fine-tuned for Hindi-English code-switching, Tamil legal terminology, or Bengali agricultural vocabulary cannot be replicated by a Silicon Valley company training on English web data.

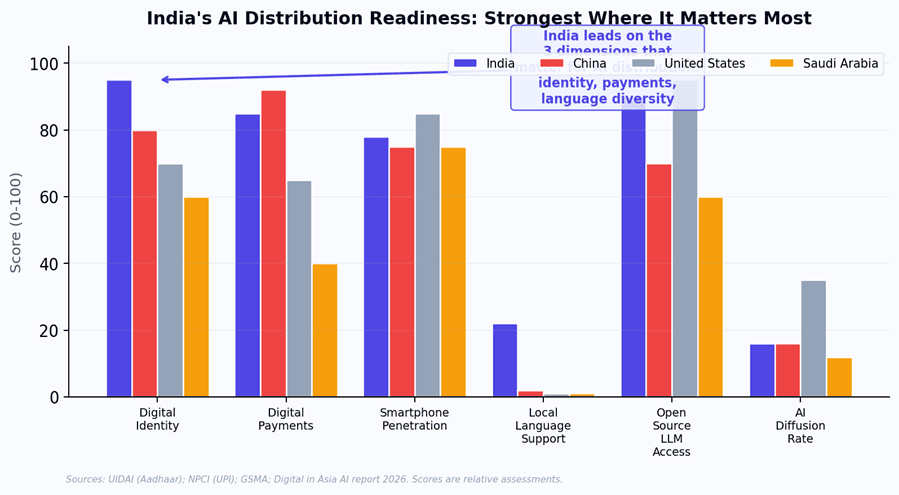

Figure 4: India's AI distribution readiness compared to other nations pursuing sovereign AI. India leads on the three dimensions that matter most: identity, payments, and language diversity.

No other country pursuing sovereign AI has all four of these layers. The UAE has money but not the user base. Saudi Arabia has ambition but not the digital payment infrastructure. France has Mistral but not 22 languages and 700 million smartphone users. India’s distribution stack is its sovereign AI - it just hasn’t been framed that way.

5. The Clock Is Ticking: Big Tech Is Already at the Gate

This is not an abstract strategic discussion. It is an urgent one. Big tech is already moving aggressively into India - and the window for Indian companies to establish distribution dominance is narrowing fast.

Microsoft committed $17.5 billion to India through 2029 - its largest investment in Asia - funding data centers in Hyderabad, Chennai, and Pune. OpenAI launched ChatGPT Go at Rs 399/month ($4.60), driving 29 million downloads in 90 days and an 800% year-over-year surge in in-app purchases. OpenAI is partnering with Tata Group for local data center buildout and with Reliance Jio’s 400-million-user mobile network for distribution. Google is offering extended Gemini Advanced trials. Perplexity partnered with Airtel. Collectively, global AI companies are running what one analyst called “the most expensive user acquisition campaign in tech history.”

But there is a crack in the strategy. As free promotional periods began expiring in 2026, conversion to paid tiers has been mixed. Churn rates are reportedly high when paywalls go up and international credit cards are required. India’s 850 million internet users are enthusiastic adopters of free AI tools - but converting them to $5-20/month subscriptions in a market where median household income is $2,100 has proven difficult.

This creates a time window. Right now, big tech cannot profitably serve Indian consumers. Per-user AI serving costs remain above Indian willingness-to-pay (as we analyzed in our Jevons Paradox piece, this convergence does not arrive until approximately 2029). Big tech is subsidizing India users with losses, hoping to monetize later. When that subsidy becomes unsustainable, they will pull back - or pivot to enterprise-only models that serve the top 2%, not the bottom 98%.

The companies that use this window to build distribution moats - domain-specific applications, vernacular language interfaces, UPI-integrated payment flows, on-device inference for offline use - will own the last mile when big tech eventually returns with sustainable economics around 2029-2030. The companies that spend this window training foundation models from scratch will find themselves competing against Llama 7, Mistral Large 3, and whatever DeepSeek releases next - with no distribution advantage to show for the years spent on model training.

“The race is not to build the best model. The race is to own the last mile before inference costs fall enough for big tech to serve India profitably.”

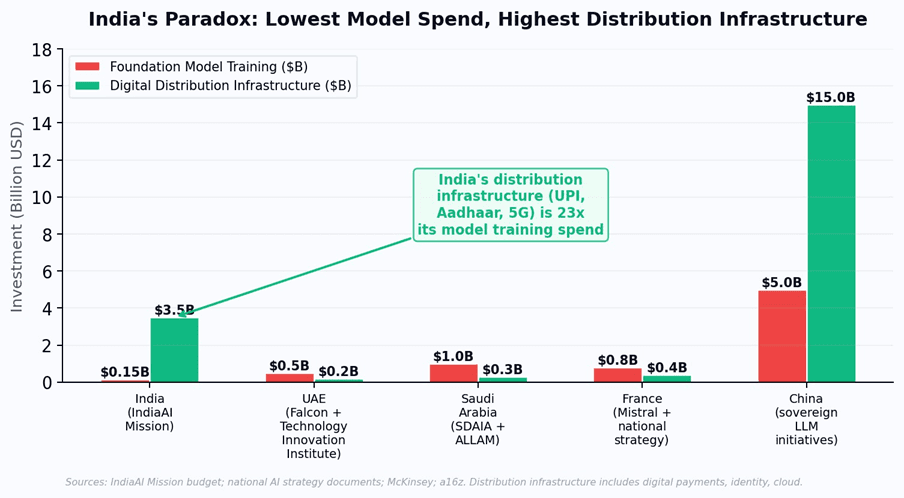

Figure 5: India paradoxically has the lowest foundation model training spend but 23x more digital distribution infrastructure than any other sovereign AI aspirant. That is the real asset.

6. The Real Sovereign AI Play: Own the Last Mile

The urgency of big tech’s advance makes the strategic question concrete: if Indian AI companies have 3-4 years before inference costs converge with Indian ARPU, what should they be building?

Not foundation models - those are a national capability investment, not a commercial moat. Sarvam, Krutrim, and BharatGen deserve continued support as strategic research infrastructure. But the commercial winners will be the companies that build the application and distribution layer connecting AI to India’s billion-plus users through India’s unique digital rails - while the window is still open.

This means: domain-specific AI applications for hiring, agriculture, education, and SME operations. Voice-first interfaces that work in Tamil, Hindi, Bengali, and Marathi. Payment integration through UPI so that AI services can monetize at Rs 10-50 per transaction, not $20/month subscriptions. On-device inference models that work offline in areas with poor connectivity. And identity integration through Aadhaar that enables personalization at population scale.

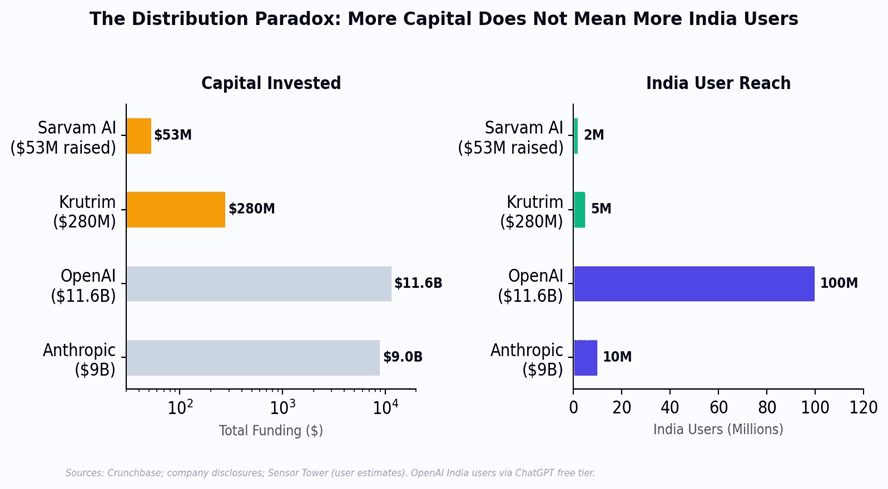

Figure 6: Capital invested vs. India user reach. OpenAI's $11.6B in funding gets 100M free-tier ChatGPT users in India - but struggles to monetize them. The last mile determines who wins.

7. Redrob’s Bet: The Android Model for AI

This is precisely why Redrob builds on open source models rather than training from scratch. A 5-model ensemble (Redrob 2B, Llama 3 8B/70B/405B, Llama 4 Maverick) running on AWS Bedrock is not a compromise. It is the Android strategy applied to AI: build the distribution layer that makes world-class AI accessible to billions, rather than building another model that joins the commoditization race.

The value Redrob creates is not in the base models - those are available to everyone. It is in the layers above: domain-specific fine-tuning for Indian HR, recruitment, and sales workflows that no global model understands natively. Multilingual intelligence across 22 languages with native code-switching. On-device inference via the Redrob 2B model that runs on $100 smartphones without an internet connection. Integration with India’s digital public infrastructure - UPI, Aadhaar, ONDC. And an intelligent routing layer that sends each query to the smallest model capable of handling it, delivering 90% of frontier performance at 5% of the cost.

India’s sovereign AI is not a foundation model. It is the distribution layer that connects AI to every citizen, in every language, through the payment system they already use, on the device they already own. The companies that build this layer will define India’s AI era - just as Google defined the mobile era not by building chips, but by building Android.